Caryn Sanchez walks through our quarterly market commentary for the first quarter of 2026.

You can listen to it here:

Her full coverage is below.

The Economy

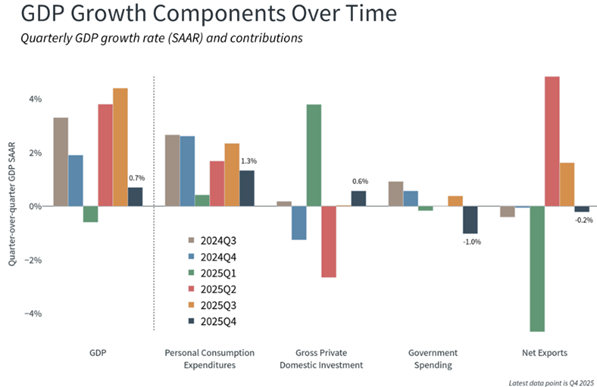

U.S. economic growth slowed in the fourth quarter. Real gross domestic product (GDP) increased at an annualized rate of 0.5% in Q4, down from 4.4% in the prior quarter. Growth was supported by higher consumer spending and investment, but those gains were partly offset by lower government spending and weaker exports (imports also declined). (Q1 GDP will be released on April 30.)

Labor market data were mixed in early 2026. Nonfarm payrolls rose by 178,000 in March after a decline of 133,000 in February. The unemployment rate held relatively steady at 4.3%, and wages increased at an annual rate of 3.5% through March 2026, indicating continued (though moderating) wage growth.

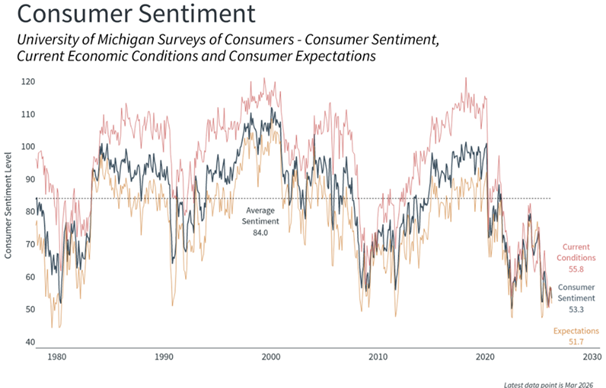

Consumer confidence weakened in March. The University of Michigan’s consumer sentiment index fell, down 6.5% from the prior 12 months. Survey respondents reported a less favorable view of current economic conditions and their personal finances, with uncertainty increasing following the start of the war with Iran.

The Consumer Price Index (CPI) rose sharply in March, up 0.9% for the month and up 3.3% over the prior 12 months. However, Core CPI, which excludes more volatile food and energy prices, was up 0.2% for the month and 2.6% over the prior 12 months.

Core PCE, the personal consumption expenditures index, is the Fed’s preferred measure of inflation. However, the monthly PCE report follows the CPI report by several weeks. The most recent numbers are from February, when Core PCE was at 3.1%; given an expected rise in inflation in March, following energy shocks from the war with Iran, February’s numbers are largely irrelevant.

Fixed Income Markets

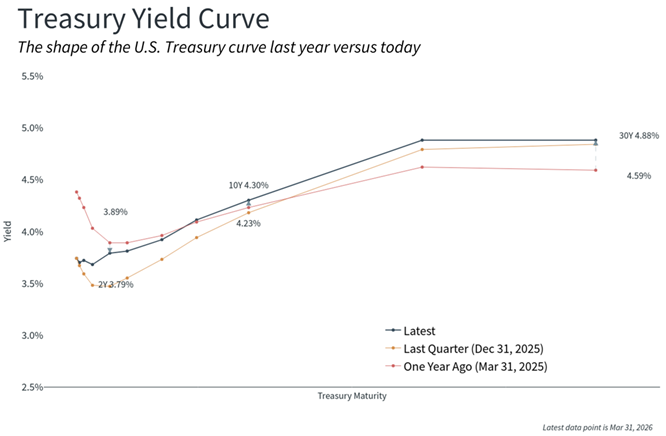

After three 0.25% rate cuts in late 2025, the Federal Reserve held interest rates steady at its March meeting, leaving the federal funds target range at 3.50%–3.75%.

Treasury yields moved higher over the quarter, with shorter-term rates rising more than longer-term rates. The yield on 2-year U.S. Treasuries ended the quarter at 3.79%, up 0.32% from the prior quarter-end. Yields on 5-year and 10-year Treasuries rose by 0.19% and 0.12% to finish at 3.92% and 4.30%, respectively. The 30-year Treasury yield increased by 0.04% to 4.88% at quarter end. Cash yields were slightly higher, rising 0.03% during the quarter and ending the period at 3.7%.

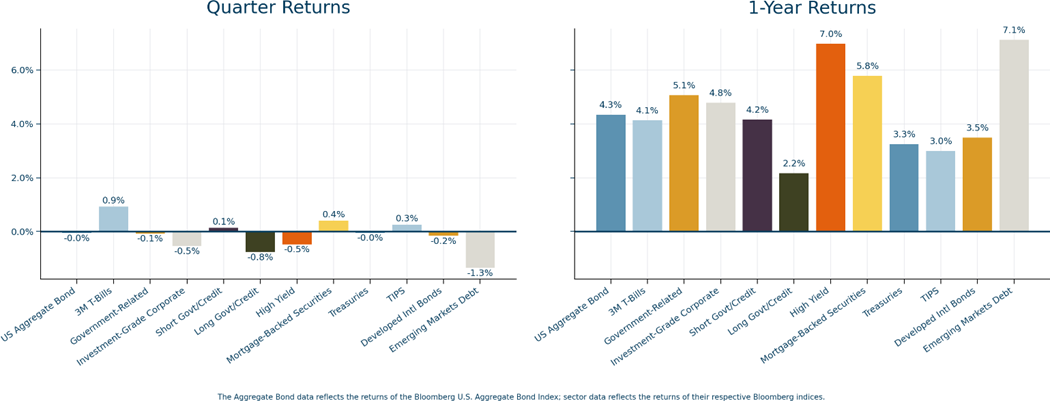

Fixed income returns were mixed in the first quarter. The Bloomberg U.S. Aggregate Bond Index, a broad measure of the U.S. investment-grade bond market, returned -0.05% for the quarter.

Performance varied across fixed income sectors during the quarter. Four sectors posted gains, led by 3-month Treasury bills (+0.9%) and mortgage-backed securities (MBS) (+0.4%). Emerging Markets Debt declined the most (-1.3%), followed by Long Government/Credit (-0.8%).

Over the past year, the Bloomberg U.S. Aggregate Bond Index returned 4.3%. All major sectors had positive returns, led by Emerging Markets Debt (+7.1%) and High Yield (+7.0%).

Equity Markets

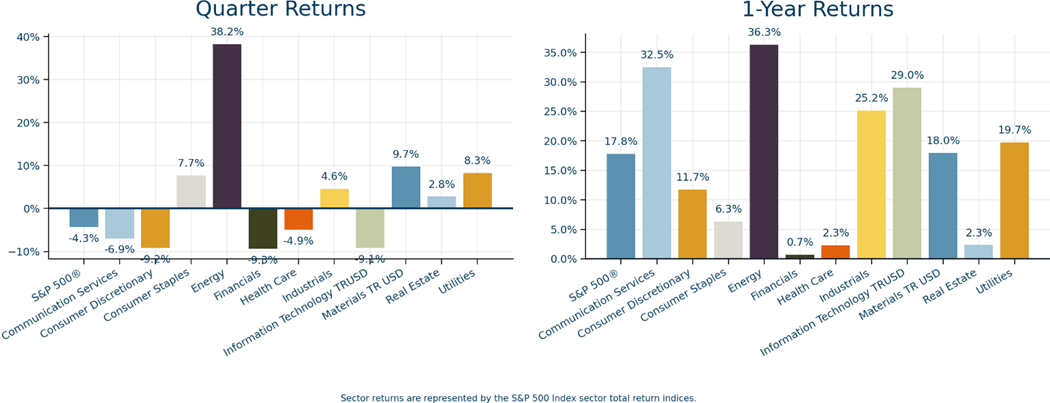

U.S. stocks declined during the quarter, with the S&P 500® Index down 4.3%. Market performance was uneven as a series of headline-driven developments in March weighed on returns, though equities rebounded on the final trading day, helping offset some of the month’s decline.

Sector results reflected shifting expectations and geopolitical developments. Following the start of the war with Iran, energy prices spiked; for the quarter, the Energy sector rose 38.2%, the strongest performance among sectors by a significant margin. In contrast, Financials, Consumer Discretionary, and Information Technology posted the largest declines, falling between 9.1% to 9.3% for the quarter.

Equity leadership also varied by investment style and company size. Value-oriented segments led: Small Value returned 5.0%, Mid Value gained 3.7%, and Large Value rose 2.1%. Growth-oriented segments lagged, with Large Growth down 9.8% and Mid Growth down 6.3%.

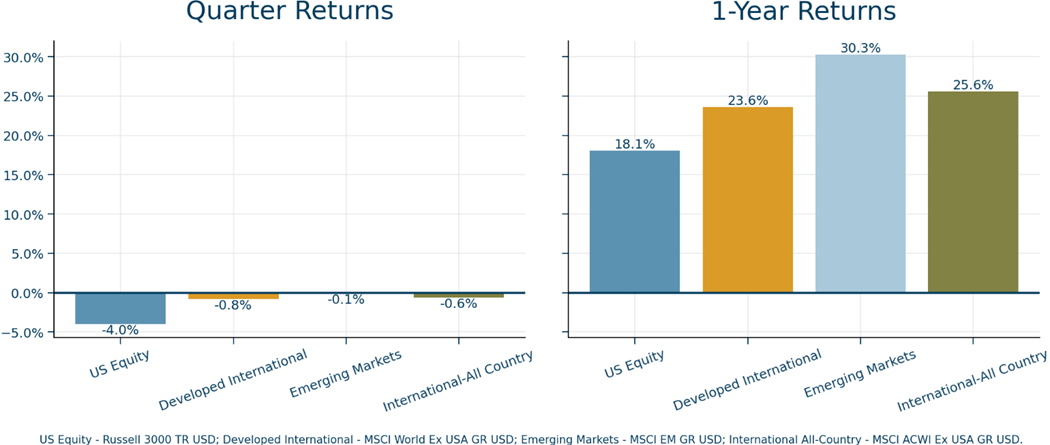

International equities also finished the quarter lower. Both developed international markets (-0.8%) and emerging markets (-0.1%) posted modest declines in absolute terms. Compared with the broad U.S. market, developed international markets and emerging markets held up better over the quarter, outperforming by 3.2% and 3.9%, respectively.

Over the one-year period, both emerging markets and developed international markets outperformed the broad U.S. market, returning 30.3% and 23.6%, respectively, versus 18.1% for the broad U.S. market.

Regional results within international equities varied widely. Emerging Markets Latin America led with a 14.7% gain for the quarter. Europe ex-UK and Emerging Markets Asia were the only regions with negative returns, down 4.0% and 1.5%, respectively.

Outlook

The S&P 500® Index ended the first quarter down 4.3%, but the headline result does not fully reflect the level of volatility during the period. In March, the war with Iran affected both equity and fixed-income markets, underscoring the role that geopolitical events can play in shaping investor sentiment and near-term market pricing. Energy and commodity prices rose sharply and remained volatile through March.

Incoming data on inflation, employment, and economic growth have been mixed, contributing to uncertainty about the path of interest rates. Bond markets have increasingly priced in the possibility that the Federal Reserve may not cut rates at all in 2026, a shift from rate cut expectations that were more common in 2025. At its March meeting, the Fed continued to project one rate cut in 2026, while also noting that the war could make inflation outcomes harder to forecast. Fed independence is also in the news as current Fed Chair Jerome Powell’s term ends in mid-May. The President has named Kevin Warsh to the post, but he faces tough confirmation hearings in the Senate. The Fed’s next meeting is scheduled for April 28–29.

Investors have also taken a more selective view of AI-related themes, focusing more closely on potential benefits and implementation costs. In recent years, market performance has often been driven by a relatively small group of large-cap companies. As expectations around technology-driven disruption continue to evolve—both in terms of opportunities and competitive pressures—performance has become more differentiated across sectors and individual companies.

Multnomah Group is a registered investment adviser registered with the Securities and Exchange Commission. Any information contained herein or on Multnomah Group’s website is provided for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Multnomah Group does not provide legal or tax advice.